As we head into the tip of the 12 months, we see that 2024 turned out to be a reasonably good 12 months for a lot of economies, particularly the U.S.

Recessions have been principally averted, inflation returned to round 2% and labor markets remained sturdy however not strained. You might say that this 12 months will finish with economies in a little bit of a “Goldilocks” state – not too sizzling, not too chilly.

Labor markets have softened however are nonetheless usually wholesome

One place the place that’s evident is in labor markets.

The previous 4 years have seen extremes for labor markets – from massive spikes in unemployment through the early a part of Covid then to traditionally tight labor markets as economies reopened, resulting in a scarcity of staff.

Now, unemployment is usually close to traditionally low ranges, however in lots of nations, it’s rising (chart beneath). That’s an indication that the provision of labor is again in step with demand for labor. In actual fact, within the U.S., the variety of jobs per individual in search of work has fallen from 2-to-1 to a way more balanced 1.1-to-1.

That’s good for corporations, because it’s getting simpler to rent employees. It’s additionally excellent news for inflation, because the tempo of wages development can also be slowing.

Jobs markets are “not too sizzling, and never too chilly.”

Chart 1: Unemployment charges are low (however principally rising)

Inflation is again close to 2% targets all over the world

Everyone knows that inflation elevated dramatically throughout Covid. That was principally as a consequence of provide chain disruptions attributable to Covid, wage pressures from tight labor markets and the Ukraine battle. The costs of products, vitality and meals all rose. Knowledge exhibits that client costs within the U.S. at the moment are round 22% increased and wages are 25% increased than earlier than Covid.

However with provide chains fastened and wage development cooling, headline inflation all over the world has fallen. It’s again round 2% in most of the world’s largest economies (chart beneath).

In brief, inflation could be very near being “good.”

Chart 2: Inflation again close to central financial institution targets

GDP development simply sturdy sufficient to keep away from recession

The primary software central banks used to get inflation again beneath management was increased rates of interest. Usually, that slows the financial system an excessive amount of, resulting in a recession, which many have been fearful about again in 2023.

Nonetheless, the information exhibits that, though development is sluggish in some locations, most nations have averted recession. Usually, nations appear to have achieved a so-called “comfortable touchdown.”

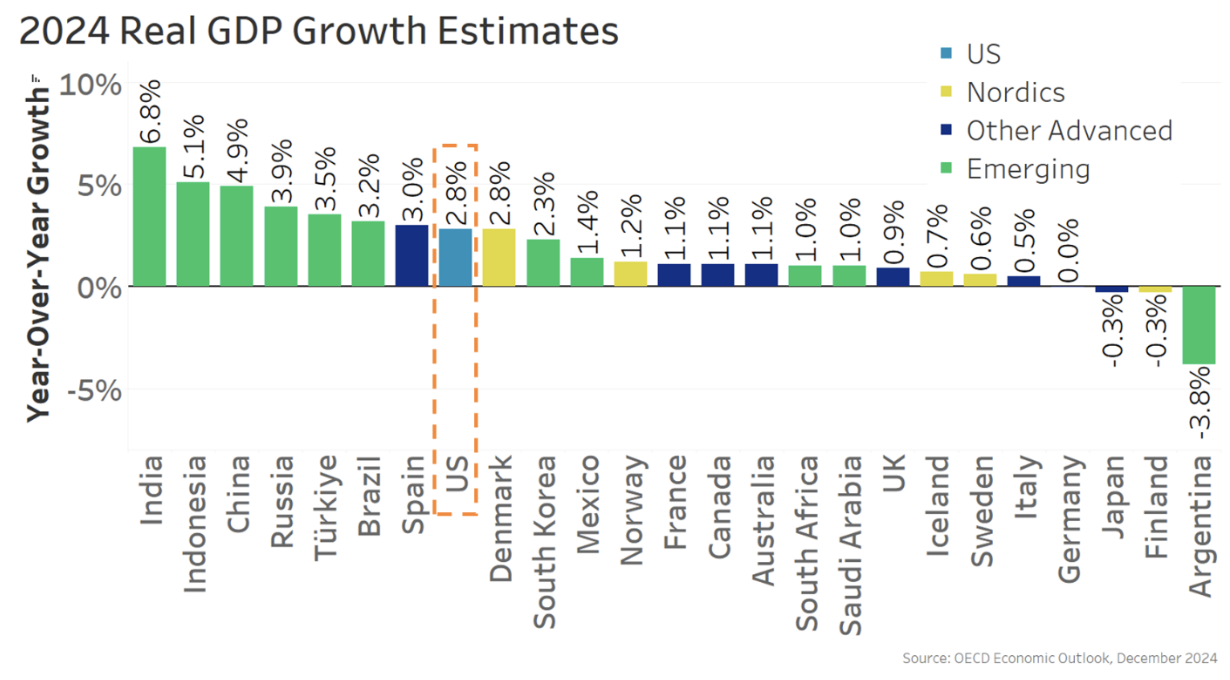

Chart 3: U.S. stands out for its sturdy development amongst superior economies in 2024

So, as we exit 2024, now we have what’s fairly near a “Goldilocks” financial system – not too sizzling, not too chilly.

Curiously, the U.S. has seen one of many strongest economies in 2024, the place now we have a 4.2% unemployment price, 2.4% inflation price, and are on tempo for almost 3% actual GDP development.

Fee cuts underway, with extra anticipated in 2025, ought to assist enhance development

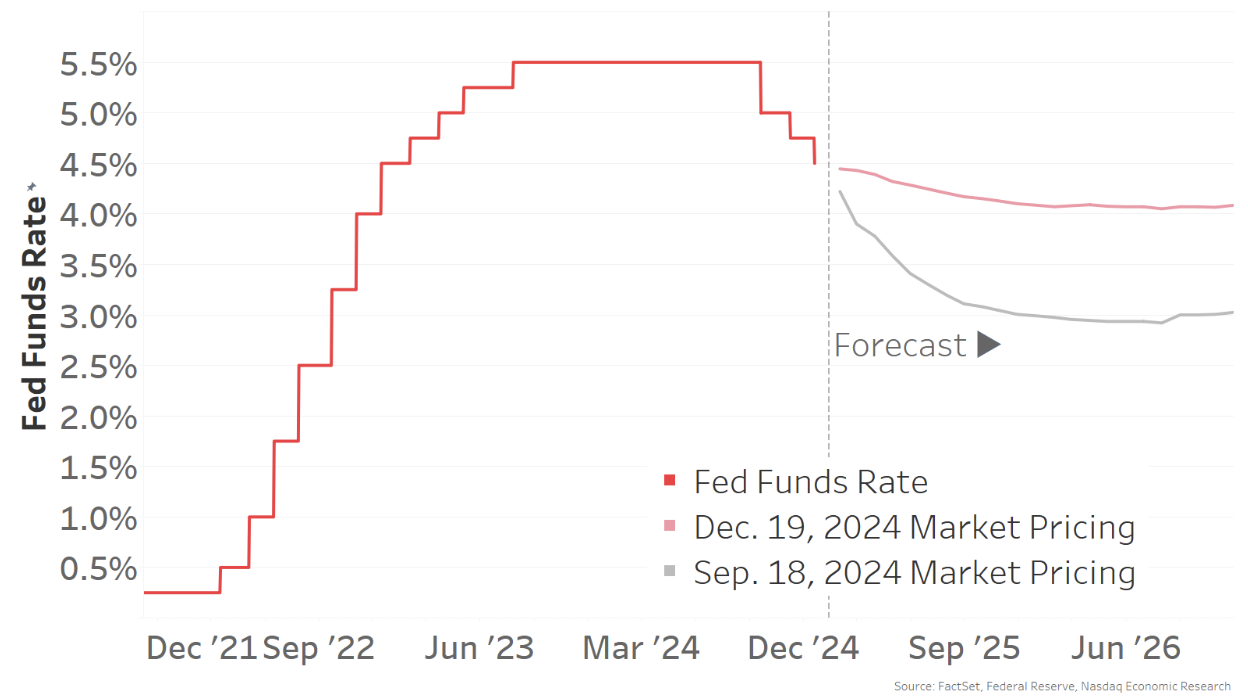

With inflation down and employment markets softer, central banks have already began to scale back charges. Based mostly on the U.S. Fed’s personal estimates, present short-term rates of interest are nonetheless at ranges which can be “restrictive” – or above the impartial price. Because of this, charges are anticipated to fall extra in 2025. The massive query is how a lot.

Simply three months in the past, markets have been pricing in a Fed funds price of round 3.0% by the tip of 2025 – a fall of round 1.5% from present ranges.

By December, rather a lot had modified. Markets now solely count on charges to fall to round 4.0%, and perhaps not attain that stage till 2026. In brief, we’re seeing charges staying higher-for-longer once more. For curiosity rate-sensitive segments of the financial system, that might have an effect on funding and development.

Chart 4: Rates of interest are falling in most nations, with extra cuts anticipated in 2025

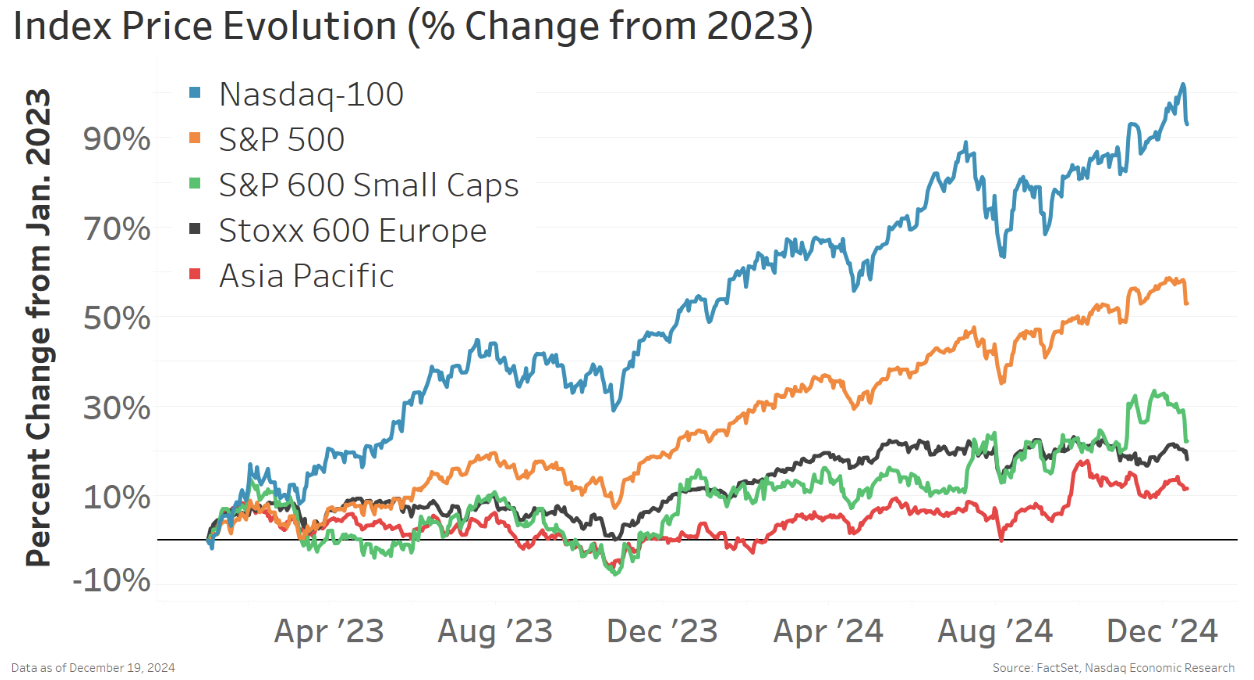

International inventory markets had a principally good 12 months in 2024

Total, 2024 was an excellent 12 months for inventory markets. Many nations noticed earnings recoveries, which, mixed with decrease rates of interest, helped push inventory valuations up.

Nonetheless, returns within the U.S. giant cap shares – and particularly for Nasdaq-100® shares – have been a lot increased than most different areas or market caps.

Chart 5: Most inventory markets are up in 2024, however U.S. mega cap noticed stronger returns

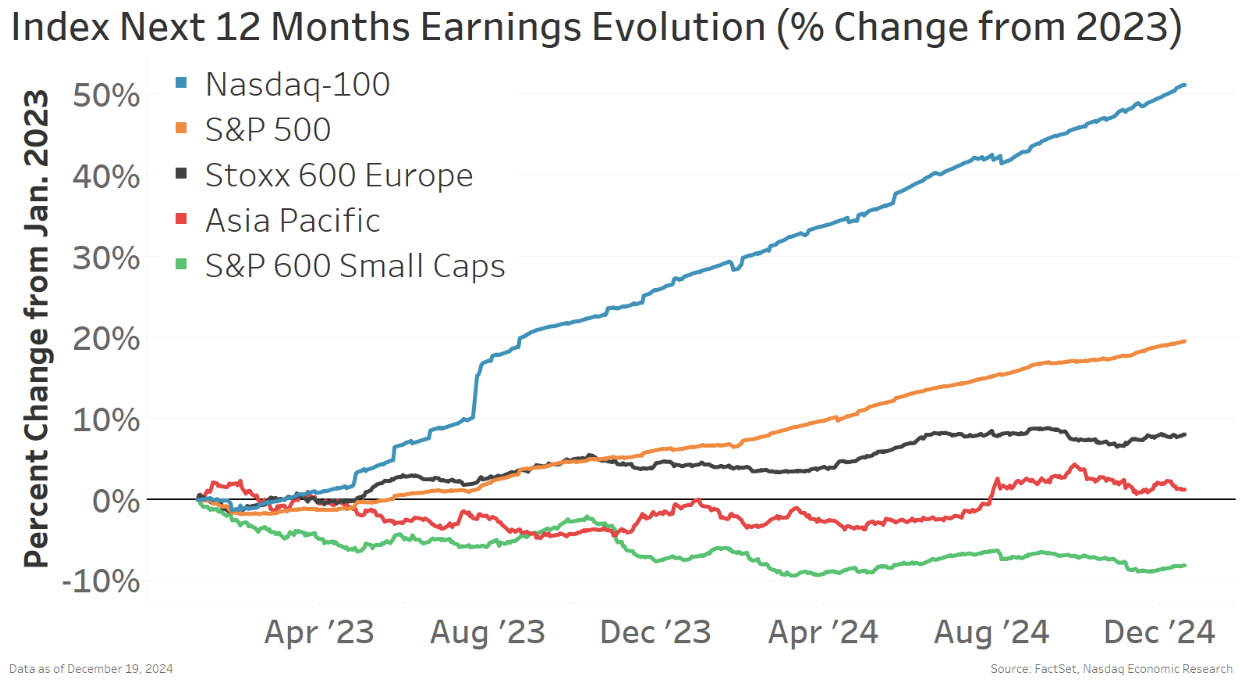

Curiously, taking a look at earnings in the identical indexes we see the identical traits.

The outperformance of the Nasdaq-100® is supported by far stronger earnings development. Whereas U.S. small caps are mired in an earnings recession.

Chart 6: Earnings traits mirror inventory returns

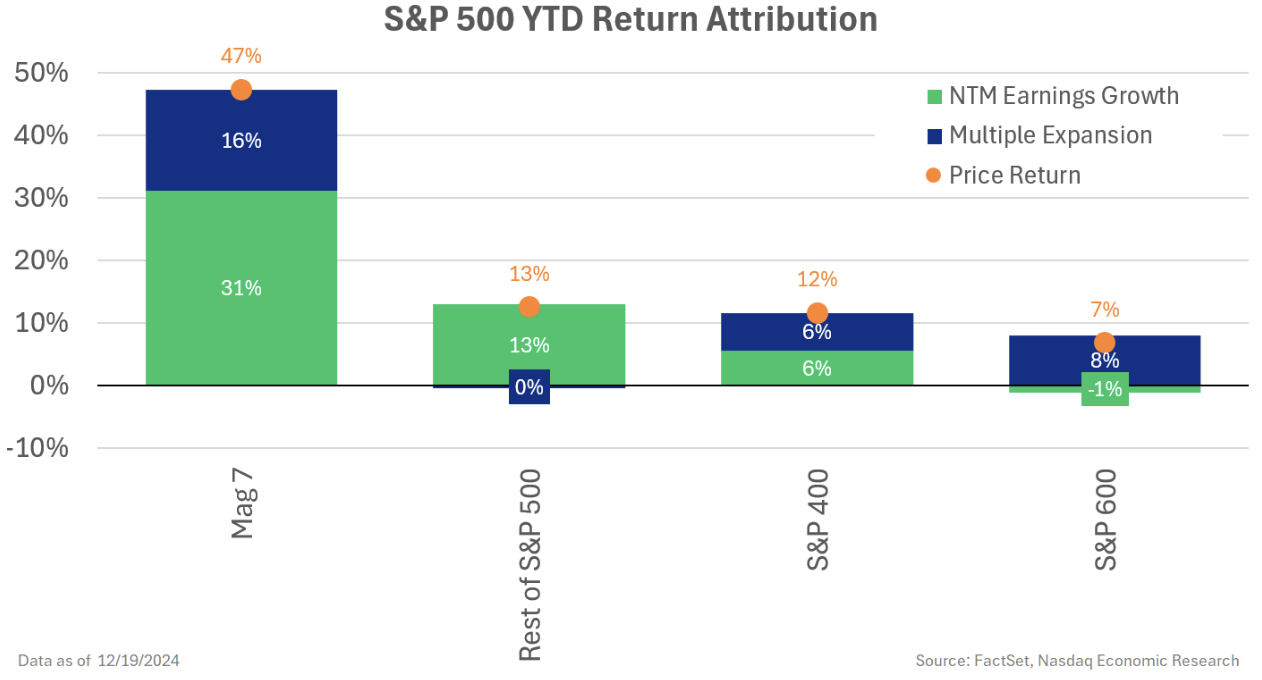

Taking a better take a look at earnings within the giant cap indexes, we see that earnings development within the S&P 500 has been pushed predominantly by the so known as “Magazine 7” shares.

All these shares are uncovered to the spending on synthetic intelligence, which some estimate is working properly over $200 billion per 12 months. Nvidia makes the GPU chips wanted for calibrating AI fashions. Amazon, Microsoft and Google all run cloud information facilities, that are key to processing all the information, and Apple, Tesla and Meta are among the many first movers utilizing AI of their merchandise.

As a result of all are Nasdaq listings, they make up a good bigger proportion of the Nasdaq-100 Index® – serving to the Nasdaq-100® outperform the broader S&P 500 index.

Chart 7: Massive-cap earnings are pushed by the Magazine 7 shares

Importantly although, as now we have progressed by way of 2024, now we have seen a broadening of the earnings restoration in the remainder of the massive cap shares.

Decrease charges can be good for small corporations

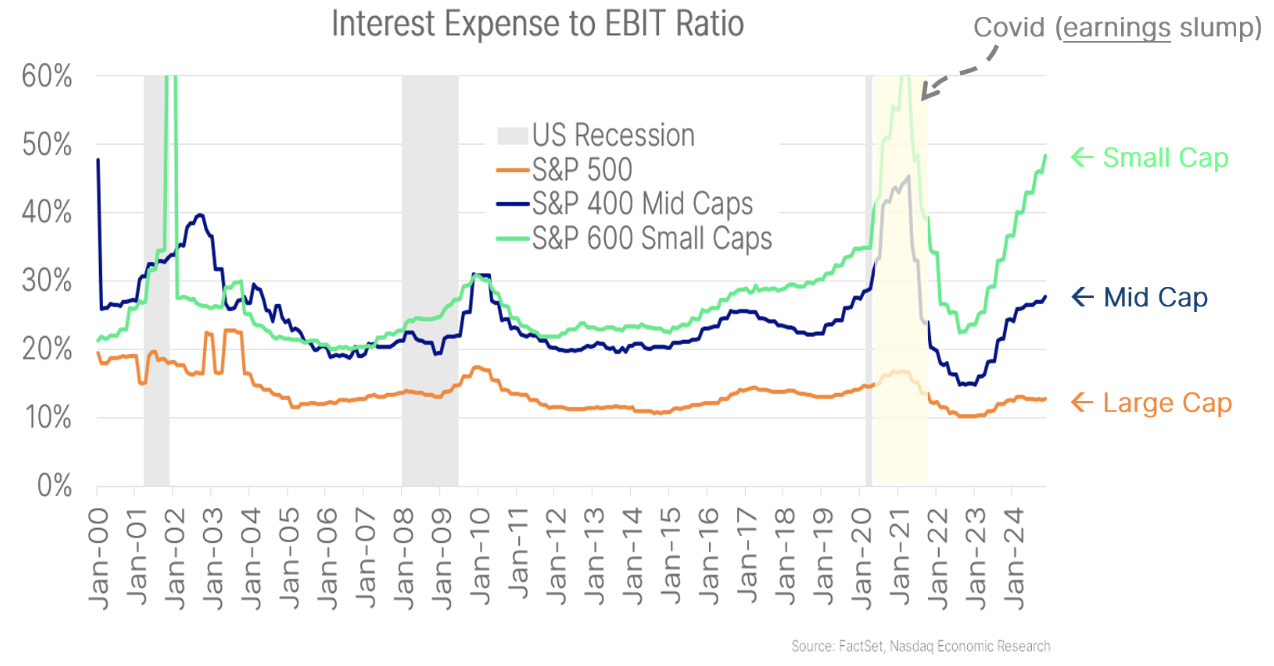

Once we take a look at the distinction between large-cap and small-cap shares, one factor stands out. Curiosity bills are lowering earnings of small cap corporations rather more than for large-cap corporations.

Some information exhibits that increased rates of interest have particularly impacted smaller companies, with curiosity expense/revenue ratios at multidecade excessive ranges. In distinction, the proportion of curiosity expense for big cap corporations is close to report low ranges – and has hardly elevated regardless of rising rates of interest.

Chart 8: Rates of interest are affecting small-cap corporations rather more than bigger corporations

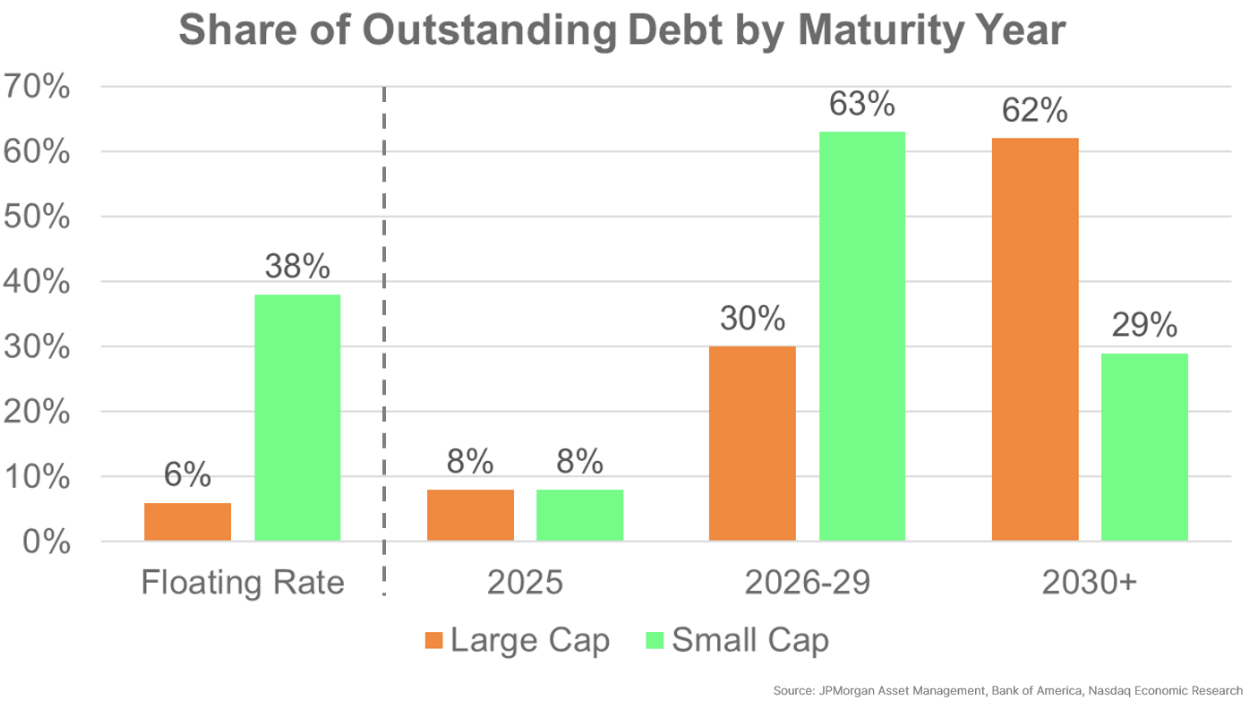

The completely different sensitivity to rates of interest is supported by taking a look at firm debt financing throughout market cap. We see that large-cap corporations have little or no floating price debt, which has insulated them from Fed rate of interest will increase. In actual fact, large-cap corporations appear to have fastened charges on the vast majority of their debt, at low charges, out to at the least 2030.

In distinction, small-cap corporations have round a 3rd of their debt at floating charges, with a big proportion of fastened price debt scheduled to refinance beginning in 2026. Clearly, small-cap corporations shall be extra impacted by charges staying higher-for-longer.

Chart 9: Small-cap corporations are rather more uncovered to increased short-term rates of interest

2025: No indicators but of client weak spot

Total, the explanation the U.S. financial system carried out so properly in 2024 was as a result of the U.S. client remained sturdy. Actual spending (adjusted for inflation) is up nearly 15% in comparison with proper earlier than Covid. That’s rather a lot higher than Europe, the place actual spending has barely elevated.

Chart 10: U.S. client spending stands out amongst different superior economies

A lot of components have helped preserve client spending development within the U.S.

Firstly, after experiencing the Credit score Disaster again in 2008, most U.S. households have now locked in long-term fastened mortgage charges. Identical to large-cap corporations, regardless of the Fed rising official rates of interest and new mortgage charges nearly tripling, the common rate of interest on excellent mortgages barely elevated – and stays round 4%. That has left more cash in individuals’s pockets – and means financial coverage has had a extra muted impression on shoppers.

Secondly, with wage good points that began within the “Nice Resignation,” after which broadened to incorporate most staff, actual wages have additionally grown. That, mixed with sturdy employment and low dangers of layoffs, has given the buyer the arrogance to maintain spending.

With rates of interest increased, even savers are incomes extra revenue.

Lastly, increased home costs have additionally left family stability sheets in a powerful place. Latest information displaying will increase in residence fairness loans (HELOCs) recommend some would possibly lastly be tapping into debt markets, permitting spending to persist.

Up to now, there are few indicators of weak spot. Bank card debt, though at new highs, is comparatively low as a proportion of revenue and family internet property. In actual fact, even the rise in unemployment (Chart 1) that the U.S. has seen is generally as a consequence of extra staff in search of jobs. Layoffs, which extra usually lead into recessions, stay close to multidecade low ranges.

Chart 11: Low layoffs have helped shoppers maintain spending

2025: Robust underlying financial system with an opportunity of uncertainty

There are loads of optimistic indicators for the U.S. financial system and the inventory market heading into 2025.

The patron stays sturdy, because of strong family stability sheets and a powerful job market.

Firm earnings are recovering. Anticipated tax cuts and looser regulation in 2025 ought to assist enhance earnings, too. Though some uncertainty exists for corporations that should take care of increased longer-term rates of interest, doable new tariffs and potential new labor shortages.

Trying on the larger image, additional rate of interest cuts, mixed with tax cuts and internet optimistic authorities spending, ought to maintain the U.S. financial system rising for at the least one other 12 months. That also needs to be good for shares.

![RAG From a Newbie to Superior: Introduction [Video]](https://toptechstocks.com/wp-content/uploads/2024/12/18089976-thumb-120x86.jpg)

{kind=link}